Inventory Management Comprehensive Guide: Your All-in-One Resource

- Updated on : October 13, 2025

- 3137 Views

- by Arun Singh Tanwar

Facebook

Facebook Instagram

Instagram Youtube

Youtube

Overview

Let’s talk about inventory management! We’ve all had moments when we wondered how companies always have their products in stock, whether it’s in their stores or online? When it comes to the business world, one thing that we can’t ignore is the importance of a good inventory management system.

Just like a superhero acts behind the scenes, good management ensures that companies don’t end up with old and dusty products, while also saving them money, time, and storage space. Sometimes, people mix up the terms “inventory management” and “inventory control,” but in this blog, we’re here to clear up all those confusions with this blog.

What is Inventory Management

Inventory management is like the magic wand that companies use to make sure they always have the right amount of products/goods they need. Whether it’s toys, gadgets, clothes, or even pizzas in a restaurant, inventory management helps companies keep track of them, ensuring they are never out of stock or never wasting the available stock. It’s all about knowing how much goods they have, when to order more, and when to sell some more.

Assume it as a well-organized treasure box, where each item is carefully counted and managed. This way, companies can avoid having too much or too little of something, which can be bad for business. It is the art of keeping a company’s stuff in check so that everything runs smoothly, without wasting the resource.

Interesting Fact: “Did you know that in 2015, businesses worldwide lost a whopping $470 billion due to overstocking and over $600 billion because of understocking? It’s like trying to guess the weather using an old umbrella – sometimes, it just doesn’t work!

Definition of Inventory Management

Let’s take a typical definition! Inventory management is a process of overseeing, managing, and controlling a company’s stock of goods and materials (inventory). It is a very crucial part of supply chain management that includes keeping track of inventory levels, raw material, finishing product, monitoring in and out movement of items, and taking strategic decisions about warehousing, ordering, and using existing stock.

The key goal of inventory management is to keep the right amount of inventory and meet customer demand while preventing aging stock, overstock circumstances.

Key Notes

- Inventory management includes administering everything from the scratch, like raw materials, to the final finished products.

- Its goal is to make sure you don’t have too much or too little stuff; it’s like finding the perfect balance.

Benefit/Importance of Inventory Management

As said before, inventory management is like having a superhero for your business. The benefit of inventory management goes beyond saving the funds, it extends to saving of time, resources, and much more. Here’s why inventory management is important:

1. Avoiding Overstock:

It helps you prevent having too much stuff on hand. Imagine if you had a closet overflowing with clothes you never wear – that’s what overstock is like for a business. It ties up money and space.

2. Preventing Stock Outs/Stock Aging:

On the flip side, inventory management makes sure you don’t run out of things when customers want them. Think of it as always having your favorite snacks available when you’re hungry.

3. Saving Money:

It helps in using your money wisely. You don’t want to spend all your allowance on toys and have nothing left for ice cream, right? Businesses want to spend just enough to meet demand without wasting money.

4. Efficient Operations:

It keeps things running smoothly. Picture a kitchen where the chef knows exactly what ingredients he has in his hand – this will make cooking much faster and efficient.

5. Happy Customers:

If you know what your customers want and when they want, they are happy. It’s like when you go to a car store that has all of your favorite cars in stock, you will end up leaving the store with a big smile.

6. Reducing Wastage:

Inventory management helps reduce waste. Imagine if a grocery store didn’t check its veggies, and they all went bad – that’s a lot of wasted food and money.

So, in simple terms, inventory management is just like having a wise wizard who makes sure you have – not too much, not too little – just the right amount of everything to keep your business strong and customers happy.

Interesting Fact: Glossier, the beauty brand, started in 2014 and sold heaps of stuff in just three months. To avoid running out, they got some inventory experts onboard. Now, they work closely with suppliers to keep things running smoothly and make more money.

Also Read: Company Valuation

Accounting for Inventory Management

Inventory is like a company’s stuff that they want to sell soon, usually within a year. But before they can show it on their financial papers, they have to count or measure it. Companies use inventory management systems to keep an eye on how much stuff they have in real-time. But there are different kinds of inventory, like:

- Raw Material: This is like the ingredients a chef uses to cook a delicious meal. Companies use raw materials to manufacture their products. For a bakery, it’s the flour, eggs, and sugar. They keep track of these ingredients in their accounting to know how much they have and how much they need to make their stuff.

- Work-In-Process: Picture this – a chef in the middle of preparing a dish. That’s work-in-process inventory. Of course this dish is not fully cooked yet, but it’s getting prepared. Companies watch WIP to know the amount of work and money it will take before producing the final product.

- Finished Goods: Think of this as the fully cooked, ready-to-eat meal. Finished goods are the products that are all set to be sold to customers. Companies count these items in their accounting to know how many they have and when they can sell them.

- Merchandise: This is like the goodies you see on store shelves. It’s ready-made stuff that stores buy and sell directly to customers. In the field of accounting, stores need to know how much their production cost and how much they have on hand.

Simply put, companies use accounting to keep track of these different kinds of stuff they have, making sure they know what’s ready to sell, what’s still being made, and what ingredients they’ve got for their products. It’s like keeping a grocery list so they never run out of what they need to run their business.

Extra Tip: IKEA, the worldwide retail giant, has a smart way to handle their stock. They set rules for when to order more stuff – like, ‘get more chairs when we’re down to 10’ and ‘don’t order more than 50 at once.’ They use fancy software to keep track of what’s selling. This helps them stay ahead in a crowded market

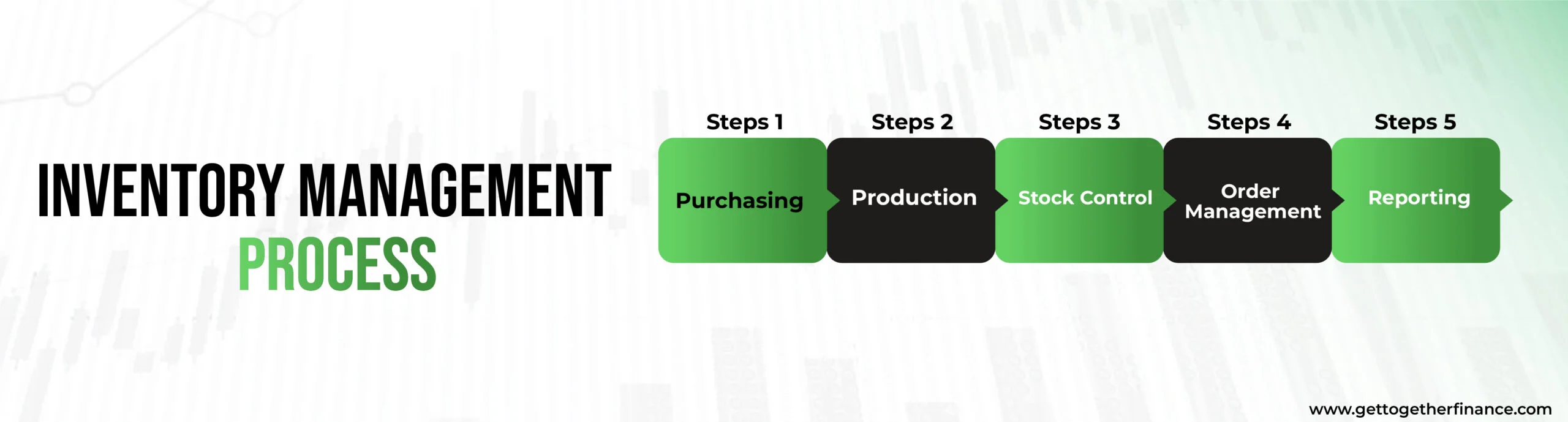

Inventory Management Process

The process of inventory management is just like well-orchestrated dance, keeping a company’s goods in perfect sync. Let’s break it down step-by-step:

1. Purchasing: The area where it all begins. Companies buy the stock of products or raw material to create or restock their inventory. It’s like going shopping for ingredients before cooking a meal.

2. Production: Well! The process of making raw material or ingredients into the final result is production. In this, sewing clothes, assembling gadgets, or baking cakes. Think of it as the cooking part of the meal prep.

3. Stock Control: Consider this as the heart of inventory management. Stock control is like putting together your toy collection, ensuring the right placement of everything. Just like this, companies also keep a track of what they have, how much they have, and where it is.

4. Order Management: Knowing about your company’s stock when customers need or buy something is order management. They check their inventory to see if all the orders can be fulfilled. It’s like taking orders at a restaurant.

5. Reporting: Just like checking your school grades at the end of the year, companies look at their reports to see how their inventory is performing. It helps them make smarter decisions about purchasing, production, and stock control.

Inventory management is a perfectly and carefully choreographed dance routine making sure everything runs smoothly. Remember, it’s all about keeping the right stuff at the right time to keep everyone satisfied.

Inventory Management Systems

An inventory management system is like a superhero tool for companies. It helps them keep tabs on their stuff as it travels from shopping and cooking to serving it on a plate, which is basically their way of managing inventory.

Example of Inventory Management

Shiva kicks off his food hamper business with a twist. He teams up with different suppliers who provide him with bulk quantities of food. But here’s the kicker: some of those goodies need to be divided and bundled into his signature hampers.

To keep things running smoothly, Shiva relies on his trusty Excel spreadsheet. It’s his go-to tool whenever he orders more supplies, assembles a hamper, or seals a deal with a customer. This spreadsheet is his inventory wizard, helping him keep tabs on his stock levels, track those pesky expiration dates, and figure out just how many hampers he can whip up. Shiva’s business success? You guessed it – it’s all thanks to his trusty spreadsheet.

Why You Need an Inventory System:

To ensure that the company has just enough stock and not too much or too little. Without a good system, things can get messy – they might end up with too many carrots or not enough potatoes for their stew. The system helps them know exactly what they need to create the perfect dish and keep everything in perfect harmony. It’s like having a secret recipe for success in business.

Periodic vs. Perpetual Inventory Systems

Periodic System: This system relies on doing regular inventory checks, like counting how many apples are left in the pantry every few months. Some popular tools for this are ERP, QuickBooks, Shopify, and Xero.

Perpetual System: This one is more real-time. It constantly keeps track of how things are coming in, going out, and getting used. It’s like always knowing how many cookies are left in the jar without having to count them every time. And when it comes to this system, LIFO ( Last-in-First-Out ) is a term you might come across.

So, whether it’s like counting your ingredients or magically knowing when to restock your pantry, the right inventory system is like having a secret recipe for business success. You can check out more about it here.

Inventory Management Methods & Techniques

When it comes to managing their stuff, companies have some cool methods up their sleeves. Let’s check them out in a simple way:

- Just-in-time (JIT): Imagine ordering your school books just before classes start. That’s what JIT is like. Companies get or make things right when they need them, so there’s no extra clutter in their storage rooms. It’s efficient, like when your mom buys groceries right before making dinner. Initially originated in Japan in the 1960s and 1970s with Toyota Motor’s support, the technique allows companies to save waste and money significantly.

- Economic Order Quantity (EOQ): EOQ is about finding the perfect amount to order. Think of it as buying just enough chocolates for a party, so you don’t run out, but you also don’t have too many leftovers that get stale. The method focuses on producing enough stock and including holding and setup costs to reduce the waste amount.

- Days Sales of Inventory (DSI): DSI tells you how fast things are flying off the shelves. It’s like knowing how quickly your favorite video game sells out in the store. Companies use this info to plan better. This method is also called the average age of inventory, days in inventory (DII), days inventory outstanding (DIO), and days sales in inventories and other ways. It grades items on the basis of its cost, demand, risks, and group items into different categories.

- ABC Inventory Management Analysis: This is like sorting your toys by how much you love them. ‘A’ toys are your absolute favorites, ‘B’ are cool but not the best, and ‘C’ toys, well, they’re okay. Companies use ABC to know which stuff is super important and which is not.

- Perpetual Inventory System: It’s like having a robot assistant always checking your toy collection. Companies use this system to instantly know how much stuff they have without manual counts. It tracks live record of purchase, sales, and inventory usages through computed ERP manufacturing software or POS systems.

- Last-in, First Out (LIFO): LIFO is like eating your newest snacks first before they get old. The companies use this technique to calculate the cost of goods sold based on the most recent purchases. It can have tax advantages but might not reflect the actual flow of inventory.

- Materials Requirement Planning (MRP): MRP is like making a shopping list before you cook a big meal. Companies use it to plan what materials they need and when to make their products. It’s all about being super organized.

- Just-in-Case Stock Control (JIC): Imagine you’re packing for a trip, and you take a few extra clothes “just in case” the weather changes. JIC is similar – companies keep extra stock on hand, just in case they run out. It’s like having spare tires in your car trunk.

- Vendor-Managed Inventory: This is when the supplier keeps an eye on your inventory for you. It’s like having a personal shopper who restocks your fridge when you’re running low on groceries.

- Cross-Docking: Think of it as a relay race for goods. Products arrive at a warehouse and are quickly sorted and shipped out without being stored. It’s like passing a baton in a race, making sure things move fast.

- Cycle-Counting: Instead of counting everything at once, cycle-counting is like checking a portion of your toys regularly. You keep counting a few every day to ensure everything’s in order over time.

- First in, First Out (FIFO): Imagine a stack of books where you always read the one on top first. FIFO is similar – the oldest items are sold or used first to ensure nothing gets too old. It’s like eating the oldest cookies in the jar first.

Use of these methods can help companies organize their stocks, save cost, and ensure that they’ve got it whenever it’s needed.

What is Inventory Control?

Inventory control means managing the stuff a business keeps in stock, like products or materials. Imagine you run a small store selling snacks. You find yourself in a situation where you can’t produce too many chips as they might go stale, but also want to have enough stock in case customers want to buy extra stock. So, you need to figure out how much to order and when to order more. Here’s what inventory control involves:

- Keeping the Right Amount: It’s like making sure you have got enough chips in stocks to sell yet not so many so it becomes old and unsellable.

- Tracking What You Have: You need to know how many chips you have in the storage room. Maybe you use a notepad to write down how many bags you sell and subtract that from what you had.

- Reordering: When you notice you’re running low on chips, you order more to restock. It’s like making sure you call the supplier before you run out.

- Avoiding Waste: You want to prevent chips from going bad or getting too old, so you sell them before they expire.

- Cost Control: You also want to be smart about the money you tie up in chips. If you have too many bags, that’s money that could be used for something else.

Hence, you can consider inventory control as the balancing act of keeping plenty of stock to meet demand while not letting it go to waste or tying up too much money in it. It’s essential for businesses of all sizes to manage their inventory effectively.

Inventory Management v/s Inventory Control

Often people get confused easily between inventory management and inventory control. Although they are cut from the same piece of cloth, there is a fine difference between both of them. In brief:

- Inventory Control focuses on the daily handling and management of goods to maintain efficiency and accuracy.

- Inventory Management involves strategic, long-term planning to align inventory with company objectives and optimize overall performance.

| Aspect | Inventory Control | Inventory Management |

| Definition | The daily management and monitoring of goods, including tracking quantities, condition, and location. | The strategic planning and decision-making process for managing a company’s entire inventory. |

| Scope | Focused on the immediate handling, organization, and optimization of current inventory. | Concerned with long-term planning, forecasting, and optimizing inventory levels over time. |

| Timing | Operational and ongoing, involving routine tasks like restocking, labeling, and quality checks. | Strategic and periodic, involving decisions about what to stock, order quantities, and seasonal adjustments. |

| Objective | To ensure efficient use of existing inventory, prevent losses, and maintain accurate stock levels. | To align inventory with company goals, minimize costs, and meet customer demand effectively. |

| Decision-Making | Involves day-to-day choices, such as reorder points, stock rotation, and quality control measures. | Involves high-level choices, like product selection, supplier negotiations, and demand forecasting |

| Primary Responsibility | Often falls on inventory managers, warehouse supervisors, or stockroom staff. | Typically managed by senior executives, supply chain professionals, and operations managers. |

Inventory Management Red Flags

Either human or inventory management, you should always spot a red flag before it starts becoming key pain in your life or business. It’s like catching a small problem before it grows into a big headache. Being proactive can save you time, money, and stress in the long run. Here are few red flags of inventory management that you ignore at your own risk:

- Excessive Stock Levels: When you have too much inventory sitting around for extended periods, it ties up your capital and storage space, leading to potential losses.

- Frequent Stockouts: Running out of essential products too often can result in lost sales and dissatisfied customers.

- Poor Inventory Turnover: If your inventory turnover rate is low, it means you’re not selling products fast enough, and you may be left with obsolete items.

- Inaccurate Records: If your records don’t match physical inventory, it can lead to confusion, errors, and financial discrepancies.

- High Holding Costs: When you spend a significant amount on storage, insurance, and maintenance for inventory, it can eat into your profits.

- Supplier Reliability Issues: Constant delays or quality problems with your suppliers can disrupt your supply chain and affect customer satisfaction.

- Unplanned Discounts and Sales: Offering frequent discounts to clear out excess inventory can impact your profitability.

- Aging Inventory: Goods that have been in stock for a long time can become obsolete, leading to losses.

- Lack of Demand Forecasting: Not accurately predicting future demand can result in overstocking or understocking.

- Manual Processes:- Relying heavily on manual tracking and ordering can lead to errors and inefficiencies.

You can take your business to new heights via just detecting red flags and taking corrective actions. Well! Of course there are other factors to consider, but hey, you finish a book by reading every chapter carefully, right!

Best Practices of Inventory Management

Using inventory management practices is just like having a fire extinguisher, it’s not what you would use everyday, but if you might need it, just keep it handy. It helps avoid the bottlenecks and risks as well as help optimize the stock control process in business.

- Regular Audits: Perform a “stock check” regularly to catch any discrepancies.

- ABC Analysis: Categorize your products into A, B, and C; from most crucial to least.

- Forecasting: Predict how much of each product you’ll need using past sales and market trends.

- Safety Stock (Atithi): Have spare snacks (inventory) at home for unexpected guests.

- First In, First Out (FIFO): Use the “first in, first out” principle, sell the old ones first.

- Vendor Relationships: Build good relationships to get better rates and quick deliveries.

- Technology: Use digital friends for inventory management software to track your orders.

- Economic Order Quantity (EOQ): Calculate right quantity for each product to reduce costs.

- Cross-Train Staff: Ensure multiple people have your back when you’re not available.

- Regular Review: Don’t just set and forget. Continuously review and adjust your inventory strategies based on changing demand, seasonal trends, and market conditions.

By following these best practices, you can keep your inventory in check, reduce costs, and ensure you have the right products available when your customers need them.

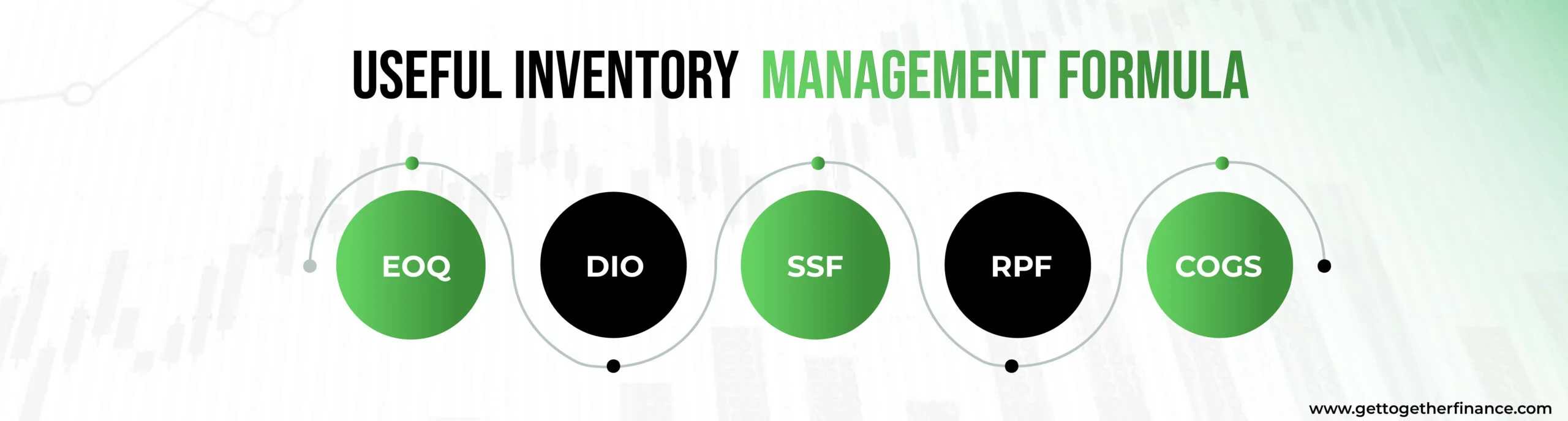

Useful Inventory Management Formula

As so far we have learned the importance, techniques, methods, and difference between inventory management and control. Let us introduce you with some inventory management formulas for new business owners. Let’s briefly break down each of these formulas to make them more approachable:

- Economic Order Quantity (EOQ) Formula: EOQ helps you figure out how much of a product to order at a time.

- D represents the cost of placing an order (like shipping and handling).

- K is how much of the product you sell in a year.

- H is the cost of holding one unit in inventory for a year (storage costs, tied-up money).

2. Days Inventory Outstanding (DIO) Formula: DIO gives you a daily view of how efficiently you manage your inventory. You calculate it by dividing the average inventory by the cost of goods sold (COGS).

- COGS is what it costs you to produce and sell your products.

- It’s important to consider industry norms when interpreting your DIO.

3. Safety Stock Formula (SSF): Safety stock is like a buffer to handle unexpected changes in demand or delivery times.

- You can calculate it by looking at your past purchase and sales order history.

4. Reorder Point Formula (RPF): This helps you determine when it’s time to reorder stock.

- Instead of relying on intuition, it’s based on factors like lead time (how long it takes to get new stock) and safety stock.

5. Cost of Goods Sold (COGS) Formula: COGS is crucial for understanding the cost of producing and selling specific goods.

- It’s a key component in inventory accounting and overall production cost calculations.

These formulas might seem complex at first, but they’re powerful tools for managing your business’s inventory effectively. They can help you save money, reduce waste, and make sure you have the right products on hand when your customers need them. If you’re ever unsure about using these formulas, consider seeking advice from an accountant or using inventory management software that can do the calculations for you.

Tim Cook on Inventory Management at Apple

Tim Cook, known for his smart inventory skills, once compared inventory to dairy products, saying, “No one wants to buy spoiled milk.” He meant that keeping too much stuff around can be as wasteful as letting milk go bad. So, managing inventory well can save a company a lot of money. It’s all about finding the right balance – having enough to meet demand but not so much that things go to waste.

The Bottom Line

Inventory management is like keeping your room tidy and your toys sorted. If you want to save your money, time, and efforts in business, you really need the exact amount of your inventories. Not too much, not too little – just enough. Whether you’re running a store or just organizing your stuff, these inventory management tips will help you keep everything in its place and avoid any surprises.

As they say – “Samay se pehle, samay par, aur samay ke baad – inventory ko sambhalna sikho!” Remember, it’s not just about counting things; it’s about making smart choices that keep your business running smoothly.

FAQs

Q1. What is aging inventory and why is it important?

A. Aging inventory means stuff that’s been sitting around in your stockroom for a while and isn’t flying off the shelves. It’s important because it ties up your money and storage space, and you don’t want your cash stuck in dusty old products. We have listed techniques to detect your aging inventory and ways to use them before the stock up.

Q2. What are the strategies that can be used to manage aging inventory?

A. You can try selling it at a discount, bundling it with other stuff, or finding a new audience for it. And if all else fails, chat with your suppliers about returning or swapping it. Oh, and don’t forget to keep a close eye on your inventory to catch aging items early. The other strategies include bundling, repackaging, promoting, or selling stuff into a different target market.

Q3. What are some effective inventory liquidation strategies?

A. You can have a big sale, offer sweet discounts, or even bundle it with popular items. Don’t underestimate the power of online marketplaces either. And hey, if all else fails, consider donating it or recycling it to reduce your losses. Recycling, local partnership, tax deduction, wholesaling, online marketplace, and bundle deals are added ways in the list, you can use to liquidate your inventory.

Now that we have already read about Inventory Management, Let’s move to the next important thing for any Business – Working Capital